Bigger, Not Better, in Private Equity Portfolios

Last week...

- The Federal Open Market Committee (FOMC) voted to keep the fed funds rate at 5.25-5.5%. As we expected, Chair Jerome Powell communicated a “hawkish pause.” Interest rates rose and market expectations for rate cuts in 2024 were lowered.

- On balance, US economic data continues to remain strong. The Atlanta GDPNow forecast for 3Q is at a blistering 4.9%.

- Stock markets pulled back slightly in the face of higher interest rates and morer estrictive Fed policy.

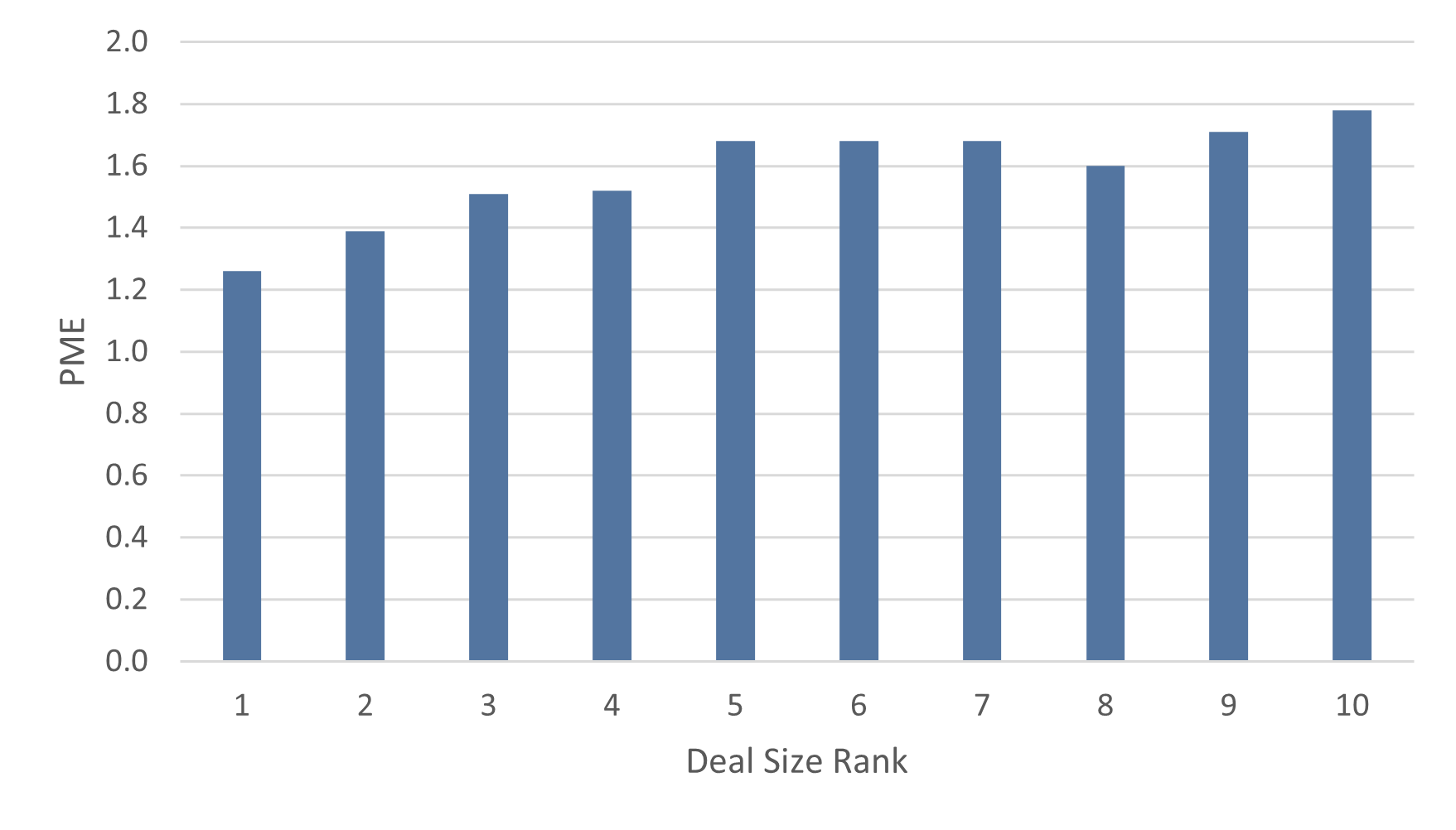

Fig. 1: Largest investments underperform others within PE funds

PME ratio of individual investments ranked by size (largest to smallest)

Earlier this month, the National Bureau of Economic Research (NBER) published “Portfolio Management in Private Equity,” a working paper analyzing the performance characteristics of individual private equity investments using a dataset of nearly 6,000 individual investments made by various funds from1999 to 2016.1 The paper delves deeper into individual variations in private equity investments and their impact on fund-level returns. They find, in part:

"General Partners (GPs) in private equity face a trade-off between focusing their skills and effort on fewer investments to earn higher returns, or investing more broadly to reduce risk through diversification... The largest investments in PE funds typically have the lowest returns on average, but are also the least risky... while GP-specific return variation (e.g., skill) only accounts for 4%-6% of the total return variation of a typical investment, it accounts for around 40% of the return variation at the fund level."National Bureau of Economic Research, Working Paper 31664, September 2023.

In other words, effectively sizing opportunities within a fund is a meaningful part of running a top performing private equity fund. We found this conclusion insightful, and it reflects our multi-decade experience as participants in the industry. We consider portfolio construction as a key part of the evaluation process and are cautious of oversized investments within any given portfolio.

Earlier this month, the National Bureau of Economic Research (NBER) published “Portfolio Management in Private Equity,” a working paper analyzing the performance characteristics of individual private equity investments using a dataset of nearly 6,000 individual investments made by various funds from 1999 to 2016.

Download Document

Download NowDisclosures & Important Information

Any views expressed above represent the opinions of Mill Creek Capital Advisers ("MCCA") and are not intended as a forecast or guarantee of future results. This information is for educational purposes only. It is not intended to provide, and should not be relied upon for, particular investment advice. This publication has been prepared by MCCA. The publication is provided for information purposes only. The information contained in this publication has been obtained from sources that

MCCA believes to be reliable, but MCCA does not represent or warrant that it is accurate or complete. The views in this publication are those of MCCA and are subject to change, and MCCA has no obligation to update its opinions or the information in this publication. While MCCA has obtained information believed to be reliable, MCCA, nor any of their respective officers, partners, or employees accepts any liability whatsoever for any direct or consequential loss arising from any use of this publication or its contents.

© 2025 All rights reserved. Trademarks “Mill Creek,” “Mill Creek Capital” and “Mill Creek Capital Advisors” are the exclusive property of Mill Creek Capital Advisors, LLC, are registered in the U.S. Patent and Trademark Office, and may not be used without written permission.