Private Equity: You Can Fix Everything but the Purchase Price (Four Charts)

Private Equity: You Can Fix Everything but the Purchase Price (Four Charts)

Private equity firms raise capital from investors, use that money to purchase companies, and then attempt to sell those companies, typically 3-5 years later, at a higher price. Once the company has been sold, the private equity firm returns the proceeds from the sale (less fees) to the investors. Historically, many private equity firms have been able to accomplish this goal and produce high returns for their investors.

However, the post-2022 era of private equity has been characterized by anemic distributions back to investors and lagging returns. These trends, generally speaking, are because private equity firms paid too much in 2021 and 2022 and cannot sell those companies into the market at a price that would earn their investors an acceptable return.

Since the private equity funds from 2021-2022 generally have 5-6 years remaining in their terms, the fund managers are holding on to the companies longer than they typically would in the hope that they will have a better opportunity to exit sometime in the next few years.

We expect the ice to thaw a bit in 2026, but do not foresee a return to normal exit volume this year. It’ll take years for the 2021 and 2022 vintages to work through the backlog.

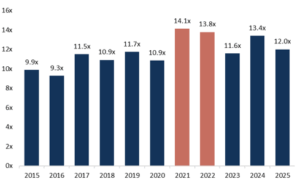

- Private equity firms paid record-high prices for the companies they purchased in 2021 and 2022 (Fig. 1)

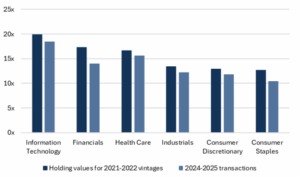

- They continue to hold those companies at prices that are higher than current market valuations (Fig. 2).

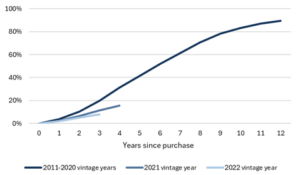

- Since PE firms are not able to exit these overvalued companies, distributions from 2021 and 2022 vintage year funds have lagged (Fig. 3)

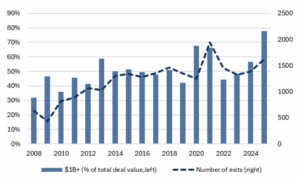

- Distributions picked up in 2025, but exits were concentrated in large companies (Fig. 4).

Fig. 1: Private equity paid record-high prices in 2021-2022 (EV/EBITDA multiples)

Source: Pitchbook, Mill Creek. As of 12/31/2025. EV/EBITDA is enterprise value divided by earnings before interest, taxes, depreciation, and amortization.

Fig. 2: Companies purchased in 2021-2022 are still marked too high (EV/EBITDA multiples)

Source: Hamilton Lane, Mill Creek. As of 10/31/2025.

Fig. 3: PE firms are holding on to 2021 and 2022 purchases longer than usual (Percentage of companies sold)

Source: Pitchbook, Mill Creek. As of 12/31/2025.

Fig. 4: Exit volume improved but nearly 80% of exits were for firms valued at 1bn or more

Source: Pitchbook, Mill Creek. As of 12/31/2025.

Disclosures & Important Information

Any views expressed above represent the opinions of Mill Creek Capital Advisers ("MCCA") and are not intended as a forecast or guarantee of future results. This information is for educational purposes only. It is not intended to provide, and should not be relied upon for, particular investment advice. This publication has been prepared by MCCA. The publication is provided for information purposes only. The information contained in this publication has been obtained from sources that

MCCA believes to be reliable, but MCCA does not represent or warrant that it is accurate or complete. The views in this publication are those of MCCA and are subject to change, and MCCA has no obligation to update its opinions or the information in this publication. While MCCA has obtained information believed to be reliable, MCCA, nor any of their respective officers, partners, or employees accepts any liability whatsoever for any direct or consequential loss arising from any use of this publication or its contents.

© 2025 All rights reserved. Trademarks “Mill Creek,” “Mill Creek Capital” and “Mill Creek Capital Advisors” are the exclusive property of Mill Creek Capital Advisors, LLC, are registered in the U.S. Patent and Trademark Office, and may not be used without written permission.