AI Jitters

Many of February’s headlines were AI fear-mongering:

- Feb 3: “Anthropic AI Tool Sparks Selloff From Software to Broader Market”

- Feb 6: “Private Credit Stocks Keep Falling as Software Wipeout Spreads”

- Feb 9: “Insurance broker stocks tumble as OpenAI approves first AI insurance app”

- Feb 10: “Wealth Manager Stocks Sink as Traders Flee Next AI Casualty”

- Feb 12: “Trucking and logistics stocks drop on release of AI freight scaling tool.”

- Feb 23: “Travel stocks tumble on AI disruption concerns”

- Feb 23: “Cybersecurity stocks drop for a second day as new Anthropic tool fuels AI disruption fears”

These industry-specific headlines culminated with an article from the Substack publication Citrini Research titled “The 2028 Global Intelligence Crisis,” that was believed to be the catalyst for a market-wide sell off on Feb 23. We didn’t find the article compelling, but the media, and some investors, are hyperventilating around AI alarmism.

Considering all the doom-and-gloom, one might be forgiven for thinking that US equity market had suffered a severe decline.

Yes, there’s potential for certain industries to be negatively impacted by AI, but those predictions are running far ahead of reality. We believe some AI perspective is in order:

- A new NBER working paper, “Firm Data on AI,” surveyed 6000 CFOs, CEOs, and executives from across the US, UK, Germany, and Australia. They found that 70% of firms actively use AI, but over 80% of firms reported no impact on employment or productivity. However, firms expect AI to boost productivity by 1.4% and reduce employment by 0.7% over the next 3 years.

- A Richmond Fed survey found similar results, which we covered here.

- There’s no AI productivity shock in the economic data yet either. Sales per employee recovered after COVID vaccines were made widely available, but have flatlined in the AI-era (Fig. 1).

- Large language model ((LLM) reliability, as tracked by Princeton University, has barely improved.

Fig. 1: Inflation-adjusted sales-per-employee

Source: Bloomberg, Mill Creek as of 2/28/2026.

In sum, AI remains unreliable and adoption has been modest.

The Market Impact

A large investment bank research shop recently wrote:

“The market now not only worries that the AI bubble will burst because AI won’t make anyone enough money, but also believes that AI will be so successful that it will result in the death of all software firms.”

It’s not that simple. AI is pretty good at writing code (although at least one study found it made experienced developers less efficient), but building a product or business is a substantial leap from writing code.

Even if we suspend reality for a moment and pretend that AI eventually functions as hyped, it is too early to confidently determine AI winners and losers.

There’s one scenario where the AI models are differentiated enough that the model providers can maintain pricing power. In that case we’d expect AI to accelerate productivity for firms, but the financial benefit would mainly accrue to the model owners (OpenAI, Anthropic, etc.).

Another likely scenario occurs if the AI models end up commoditized (undifferentiated) and users are happy to switch between Chat GPT, Claude, Grok, etc. The cost of compute will drop to marginal cost of production and the overall financial benefits will accrue to the users of AI, including software companies. In this scenario, the AI model builders struggle to recoup their investment costs.

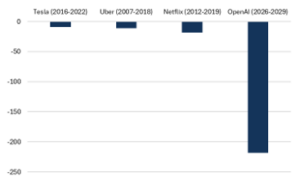

In both cases the broader economy benefits and the impact on consumer prices depends on the cost of compute, which remains quite high and is currently being subsidized to promote usage. Uber burned 18.2B in cash between 2016-2022 before becoming cash flow positive. OpenAi is planning to burn $218bn over the next four years (Fig. 2). Compute isn’t free (hence the ChatGPT announcement that they are testing ads) and consumer subsidies will eventually have to end, something the Citrini article completely ignored.

Fig. 2: Free cash flow burn

Source: Bloomberg, Mill Creek as of 2/28/2026.

Here’s our bottom line:

To reiterate a message from our 2026 year ahead: The economic backdrop remains positive for risk assets, but a lot of positive news has already been priced in.

Valuations are important in a late cycle environment and we encourage investors to remain underweight the high-valuation parts of the market that are prone to disappointment. Software stocks were trading at a 40 price-to-earnings ratio (P/E). Now they trade at a 24 P/E, versus 21.5 P/E for the overall US market. We continue to prefer US small cap to US large cap growth, and remain neutral to US vs. international. We also continue to see opportunities for equity-like returns in asset-based private lending, specialty finance, and value-add real estate.

Disclosures & Important Information

Any views expressed above represent the opinions of Mill Creek Capital Advisers ("MCCA") and are not intended as a forecast or guarantee of future results. This information is for educational purposes only. It is not intended to provide, and should not be relied upon for, particular investment advice. This publication has been prepared by MCCA. The publication is provided for information purposes only. The information contained in this publication has been obtained from sources that

MCCA believes to be reliable, but MCCA does not represent or warrant that it is accurate or complete. The views in this publication are those of MCCA and are subject to change, and MCCA has no obligation to update its opinions or the information in this publication. While MCCA has obtained information believed to be reliable, MCCA, nor any of their respective officers, partners, or employees accepts any liability whatsoever for any direct or consequential loss arising from any use of this publication or its contents.

© 2025 All rights reserved. Trademarks “Mill Creek,” “Mill Creek Capital” and “Mill Creek Capital Advisors” are the exclusive property of Mill Creek Capital Advisors, LLC, are registered in the U.S. Patent and Trademark Office, and may not be used without written permission.