Looking for Alpha in All the Wrong Places

Hendrik Bessembinder, Professor of Finance at Arizona State University, recently updated his long-term stock market research in a paper titled “One Hundred Years in the U.S. Stock Markets.” His update provides a good excuse for us to revisit our philosophy behind equity market investing.

Bessembinder finds that while the stock market has created enormous wealth over the long term, wealth creation was extremely concentrated in a few stocks. Nearly 60% of publicly traded firms destroyed wealth, whereas only 46 firms (out of nearly 30,000) accounted for 50% of wealth creation over the last 100 years.

One might hear that conclusion and think “great, all I need to do is pick the best stocks, hold them, and I’ll be the next Warren Buffett.” In fact, a common investment trope is to be concentrated and long-term. It implies skill, and confidence, in investment selection, which everyone thinks sounds great. Unfortunately, concentrated and long-term is more likely to lead to sustained underperformance in public equities than significant outperformance.

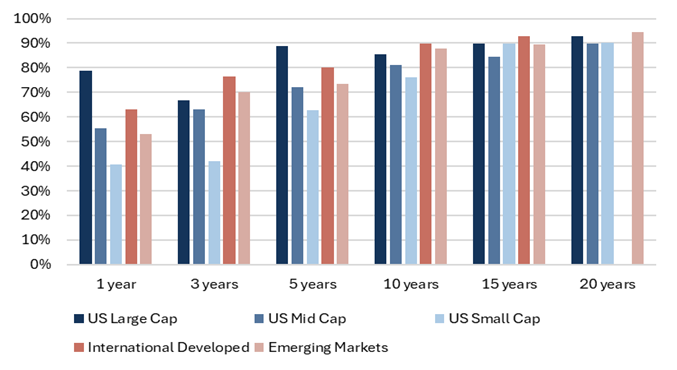

When it comes to stock market performance, missing the winners is far worse than holding the losers, and most stock-pickers miss the winners. The vast majority of professional equity managers have underperformed simple indexes, including small cap and international equity managers over 3, 5, 10, 15, and 20 years (Fig. 1).[1]

Fig. 1: Percentage of active equity managers underperforming their indexes

Source: S&P SPIVA US Scorecard, Mill Creek. As of 12/31/2025.

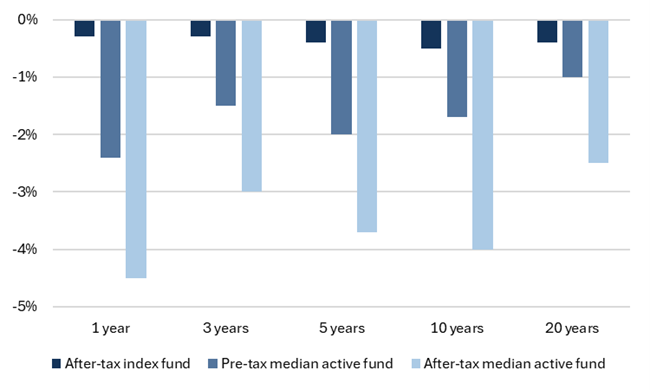

To make matters worse, outperforming managers rarely outperform by enough to cover their taxes.[2] Tax-drag cost US active equity fund investors 1.6% per year between 2015-2025 (Fig. 2), a period in which fewer than 2% of US equity managers were able to outperform net of fees and taxes.[3] Needle, meet haystack.

Fig 2: Annualized performance versus the S&P 500

Source: S&P SPIVA After-Tax Scorecard, Mill Creek. As of 12/31/2024.

Not all is lost! Low-fee, tax efficient index funds, combined with some evidence-based allocation nudges (we’re currently overweight US small cap versus US large and international), are hard to beat. However, we can add additional value (aka tax alpha) through tax-loss harvesting.

At a high level, we utilize strategies that seek to track a market index, like the S&P 500, while also generating tax losses along the way. The magnitude of expected losses ranges by strategy but tends to fall between 0.5-5% of invested assets annually. These losses can then be used to offset realized gains in other parts of the portfolio, creating real value for a taxable investor.

[1] https://www.spglobal.com/spdji/en/documents/spiva/spiva-us-year-end-2025.pdf

[2] https://www.researchaffiliates.com/content/dam/ra/publications/pdf/670-is-your-alpha-big-enough-to-cover-its-taxes.pdf

[3] https://www.spglobal.com/spdji/en/documents/spiva/spiva-after-tax-scorecard-year-end-2024.pdf

Disclosures & Important Information

Any views expressed above represent the opinions of Mill Creek Capital Advisers ("MCCA") and are not intended as a forecast or guarantee of future results. This information is for educational purposes only. It is not intended to provide, and should not be relied upon for, particular investment advice. This publication has been prepared by MCCA. The publication is provided for information purposes only. The information contained in this publication has been obtained from sources that

MCCA believes to be reliable, but MCCA does not represent or warrant that it is accurate or complete. The views in this publication are those of MCCA and are subject to change, and MCCA has no obligation to update its opinions or the information in this publication. While MCCA has obtained information believed to be reliable, MCCA, nor any of their respective officers, partners, or employees accepts any liability whatsoever for any direct or consequential loss arising from any use of this publication or its contents.

© 2025 All rights reserved. Trademarks “Mill Creek,” “Mill Creek Capital” and “Mill Creek Capital Advisors” are the exclusive property of Mill Creek Capital Advisors, LLC, are registered in the U.S. Patent and Trademark Office, and may not be used without written permission.