Don’t Worry Yet: 2026 Isn’t Partying Like It’s 1999

Don’t Worry Yet: 2026 Isn’t Partying Like It’s 1999

The S&P 500 is up 28% over the last year and nearly 100% since ChatGPT was released in November 2022, resulting in a flurry of comparisons to the dot-com era. It is not a good comparison.

- Investors bid up stock prices during the 1995-2000 dot-com period well in excess of expected earnings. From the time Netscape Navigator was released in late 1994 until the bust, the S&P 500 increased 250% versus only an 80% increase in 12-month forward earnings expectations (Fig. 1).

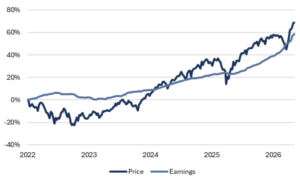

- This time around, S&P 12-month forward earnings and the index have appreciated approximately the same (60%) since 2021, and stock prices have actually lagged earnings revisions since January of 2025 (Fig. 2).

- Excluding rebounds out of recessions, expected twelve-month forward earnings per share for the S&P 500 have risen faster over the last year (+29%) than at any point since the early 1990s (Fig. 3).

The dot-com era was a time of exuberance about potential earnings that never materialized. The current rally is exuberance about actual earnings that are accelerating faster than market participants had expected. There’s a party, but it’s not 1999 redux.

Fig. 1: 1995-2000 S&P 500 total return and 12-month forward earnings change (%)

Source: Bloomberg, Mill Creek. As of 5/21/2026.

Fig. 2: 1995-2000 S&P 500 total return and 12-month forward earnings change (%)

Source: Bloomberg, Mill Creek. As of 5/21/2026.

Fig. 3: Estimated earnings per share growth (S&P 500, year-over-year)

Source: Bloomberg, Mill Creek. As of 5/21/2026. Data shows 12-month forward earnings per share growth over annual periods.

Disclosures & Important Information

Any views expressed above represent the opinions of Mill Creek Capital Advisers ("MCCA") and are not intended as a forecast or guarantee of future results. This information is for educational purposes only. It is not intended to provide, and should not be relied upon for, particular investment advice. This publication has been prepared by MCCA. The publication is provided for information purposes only. The information contained in this publication has been obtained from sources that

MCCA believes to be reliable, but MCCA does not represent or warrant that it is accurate or complete. The views in this publication are those of MCCA and are subject to change, and MCCA has no obligation to update its opinions or the information in this publication. While MCCA has obtained information believed to be reliable, MCCA, nor any of their respective officers, partners, or employees accepts any liability whatsoever for any direct or consequential loss arising from any use of this publication or its contents.

© 2025 All rights reserved. Trademarks “Mill Creek,” “Mill Creek Capital” and “Mill Creek Capital Advisors” are the exclusive property of Mill Creek Capital Advisors, LLC, are registered in the U.S. Patent and Trademark Office, and may not be used without written permission.