Inflation Is Still a Problem

Inflation Is Still a Problem

Inflation jumped in April and continues to represent, in our opinion, a significant challenge for the Federal Reserve.

- The Consumer Price Index was up 3.8% year-over-year as of April. The 3-month annualized increase was 7.3% (Fig. 1).

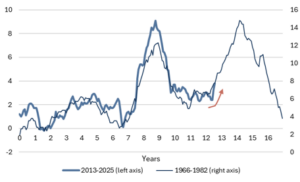

- Inflation continues to follow down the path of the 1966-1982 “twin-peaks” pattern (Fig. 2).

- The magnitude of inflation is lower today than it was in the 1970s, but the Fed might be facing a repeat of the lessons from that decade. Repeated economic supply shocks (e.g. COVID, tariffs, energy prices) and elevated inflation expectations from households make it hard to “defeat” inflation without a recession.

The 10-year Treasury yield is once again flirting with 4.6% and the Fed has failed to meet its inflation goal for over five years. Economic growth remains strong, the labor market is solid, but inflation is too high.

Accordingly, we continue to believe that the Fed will struggle to find a credible rationale for rate cuts in 2026. Rate hikes, instead of cuts, are an increasingly likely possibility.

Fig. 1: US Consumer Price Index (CPI)

Source: Bloomberg, Mill Creek. As of 5/13/2026.

Fig. 2: US CPI Twin Peaks redux?

Source: Bloomberg, Mill Creek. As of 5/13/2026. Chart shows year-over-year CPI % change for the periods specified.

Disclosures & Important Information

Any views expressed above represent the opinions of Mill Creek Capital Advisers ("MCCA") and are not intended as a forecast or guarantee of future results. This information is for educational purposes only. It is not intended to provide, and should not be relied upon for, particular investment advice. This publication has been prepared by MCCA. The publication is provided for information purposes only. The information contained in this publication has been obtained from sources that

MCCA believes to be reliable, but MCCA does not represent or warrant that it is accurate or complete. The views in this publication are those of MCCA and are subject to change, and MCCA has no obligation to update its opinions or the information in this publication. While MCCA has obtained information believed to be reliable, MCCA, nor any of their respective officers, partners, or employees accepts any liability whatsoever for any direct or consequential loss arising from any use of this publication or its contents.

© 2025 All rights reserved. Trademarks “Mill Creek,” “Mill Creek Capital” and “Mill Creek Capital Advisors” are the exclusive property of Mill Creek Capital Advisors, LLC, are registered in the U.S. Patent and Trademark Office, and may not be used without written permission.