Notes on Operation Epic Fury

Notes on Operation Epic Fury

Our original market commentary for March focused on the AI-driven market volatility we observed last month. We’ll publish that article later this week, but Operation Epic Fury takes precedence today.

We’ll avoid the temptation to prognosticate too much on the impact at such an early stage of the operation, but have a few economic and market observations:

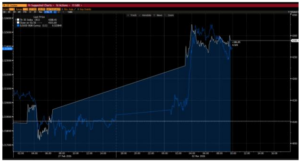

1. How is the operation going? Based on the reaction of the Tel Aviv stock exchange and the Shekel, we’d suggest pretty good so far (Fig. 1).

2. The “flight to safety” trade Monday morning was expected. US Treasuries, the US dollar, Swiss franc, and gold opened higher.

On this point, the US dollar and US Treasuries both appreciated as diplomatic talks with Iran progressed through February. Were those markets pricing-in an increasing inevitability of conflict? If so, we could see a “buy the rumor, sell the news” trade (higher rates, weaker dollar) after the initial reaction wears off.

3. Current reports indicate that the Strait of Hormuz has been effectively shut and we expect oil prices to open higher on Monday.

When you’re reading news about oil prices, remember that all oil prices are based on a specific time, location, and quality, even if that information isn’t in the article. US oil prices are typically quoted as West Texas Intermediate (WTI), which means the price for physical delivery, a certain number of months in the future, in Cushing, Oklahoma. The rest of the world quotes oil prices as Brent crude, which is the price of seaborn crude.

WTI and Brent generally trade together, but if the Strait of Hormuz is closed we should expect the spread between WTI and Brent to widen significantly. We simply point this out for anyone thinking about using oil funds to speculate on price movements.

Whether prices remain elevated is an open question. OPEC + has announced output hikes, and the Trump Administration could use releases from the Strategic Petroleum Reserve to keep prices subdued in the US. Finally, to borrow a message from our 2026 outlook, all shortages lead to gluts. An oil price spike will inevitably lead to additional supply and eventually a glut.

4. The economic impact, if anything, will be a nudge further toward stagflation. Higher commodity prices constitute a supply shock. On the margin, that means higher inflation and slower growth. Economic growth is reasonably strong in the US and around the world, but inflation remains a touch too high.

A sustained conflict in the Middle East could lead to higher energy prices, but 2026 is not 1979, and true stagflation is an unlikely outcome. In the near term the Fed is likely to lean toward lower rates and supporting growth in the face of an ongoing conflict. Higher inflation could be a headwind to additional rate cuts in the second half of 2026.

We intentionally build portfolios for a wide range of economic regimes. That construction includes enough cash and yield to look beyond periods of market stress and distress in order to make decisions based on fundamentals.

While sentiment can be a fuzzy concept, we don’t believe it is a stretch to say that many investors are either skeptical of the current environment or downright bearish. February’s market volatility was concentrated in parts of the equity market with high valuations (e.g. software, trucking), but Operation Epic Fury could be a catalyst for a broader, sentiment-driven, sell-off. That’s not our base case, but if it happens we’ll likely recommend waiting for the sell-off to subside and then buying the recovery.

For now, we remain constructive on risk assets against a backdrop of low interest rates and strong economic growth. We’ve signaled that we want to keep a tight leash on risk, but we’re not ready to yank that leash back quite yet.

Fig. 1: Tel Aviv Stock Market (White) and Shekel/USD (Blue)

Source: Bloomberg, Mill Creek. As of 10am EST 03/02/26.

Disclosures & Important Information

Any views expressed above represent the opinions of Mill Creek Capital Advisers ("MCCA") and are not intended as a forecast or guarantee of future results. This information is for educational purposes only. It is not intended to provide, and should not be relied upon for, particular investment advice. This publication has been prepared by MCCA. The publication is provided for information purposes only. The information contained in this publication has been obtained from sources that

MCCA believes to be reliable, but MCCA does not represent or warrant that it is accurate or complete. The views in this publication are those of MCCA and are subject to change, and MCCA has no obligation to update its opinions or the information in this publication. While MCCA has obtained information believed to be reliable, MCCA, nor any of their respective officers, partners, or employees accepts any liability whatsoever for any direct or consequential loss arising from any use of this publication or its contents.

© 2025 All rights reserved. Trademarks “Mill Creek,” “Mill Creek Capital” and “Mill Creek Capital Advisors” are the exclusive property of Mill Creek Capital Advisors, LLC, are registered in the U.S. Patent and Trademark Office, and may not be used without written permission.