Profits Without People

Profits Without People

The 19th century French Philosopher Auguste Comte argued that “demography is destiny.” If true, our destiny is about to hit an inflection point.

Economic growth, at its core, is the combination of the number of hours people work in an economy (the size of the labor force) and how efficiently they work (their productivity). This simple construct makes it clear there are two main ways an economy can grow:

- Population growth (natural or through immigration), and

- Productivity growth.

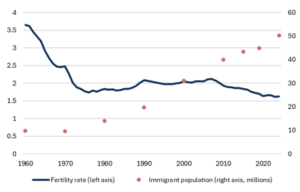

The US has experienced population growth since WW2. While the US fertility rate has been at or below replacement level (2.1 births per woman) since the early 1970s, net positive immigration offset fertility declines and resulted in continuous, if low, population growth (Fig. 1).

Fig. 1: US fertility rate and immigration

Source: FRED, Mill Creek. As of 2024 (most recent data).

However, the US fertility rate has fallen to 1.53 babies per woman,1 and deaths are expected to exceed births in 2030. This means that net immigration will drive population growth, or declines, in the US from 2030 forward.

Can immigration fill the population gap? The US Congressional Budget Office expects net immigration to return to 1.2mn individuals per year by 2036, which, if it happens, will keep US population growth positive until around 2056. We’re not on track to reach those numbers this year. The US Census Bureau projects net immigration of +321,000 for 2026,2 but some forecasters, like the Brookings Institution, believe that net immigration has already turned negative.3 Regardless of which estimates are correct, US population growth has slowed to a trickle, job growth has (appropriately)4 slowed to a trickle, and productivity growth is in the driver’s seat for economic growth.

1 https://www.cbo.gov/publication/61994

2 https://www.census.gov/newsroom/blogs/random-samplings/2026/01/historic-decline-in-net-international-migration.html

3 https://www.brookings.edu/articles/macroeconomic-implications-of-immigration-flows-in-2025-and-2026-january-2026-update/

4 Researchers at the Federal Reserve Bank of Dallas believe the “break-even” job growth, the number of jobs we need for the unemployment rate to remain steady, has likely fallen to 30k per month, and might even be negative.

Fig. 2: US productivity growth, 5-year rolling average.

Source: Bloomberg, Mill Creek. As of 3/31/2026.

Fortunately, we’ve also been the beneficiary of consistent productivity growth that has averaged just over 2% annualized for six decades (Fig. 2) and has been above average, closer to 2.5%, post-COVID. Absent these productivity gains US economic growth would have been much more anemic.

Our lack of population growth coincides with a native population that is rapidly growing older. The median worker in the US is 42 years old, compared to 35 years old in the early 1980s and the labor force participation rate has dropped from above 67% in the late 1990s to 62% today, primarily because of aging.

Nursing homes and data centers

US GDP growth remains resilient despite stalled labor market growth (Fig. 3). Why, and what does this mean for the economy and investments?

Fig. 3: Trailing 12-months GDP growth and Non-farm Payroll Growth

Source: Bloomberg, Mill Creek. As of 4/29/2026.

Economic growth has been resilient because productivity growth has averaged 2.8% in the US over the last three years versus only 1% from 2010 to 2020. Our view is that recent productivity growth has primarily come from bloated firms laying off unproductive workers instead of actual gains from artificial intelligence, but firms remain optimistic that the trillion dollars invested in AI will eventually lead to tangible efficiency gains for their employees (See: Firms Are Investing in AI, but the Impact Is Uncertain Thus Far).

In regard to market impact, we’d start by asking, “what do retirees buy?” and then thinking about the impact of labor constraints on the firm. If the investment requires more people for success, whether it be consumers or workers, challenging times are ahead. Homebuilders, expensive durable goods, and educational institutions are likely to face headwinds. On the other hand, if the firm can grow without population growth, then it is well positioned for our profits without people destiny.

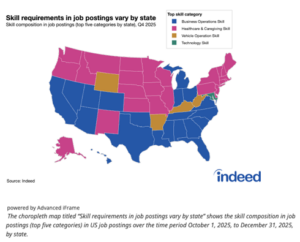

Healthcare certainly remains at or near the top of the list for growth tailwinds. As we discussed in our quarterly outlook, healthcare has been responsible for 100% of net job growth over the last three years and a recent Indeed report indicated that “Healthcare and Caregiving Skill” was the top skill category for job postings in 25 states (Fig. 4)

Fig. 4: Healthcare has become a top-skill requirement in job postings

Source: Indeed. https://www.hiringlab.org/2026/04/09/skill-set-match-in-job-postings/

We also believe that labor shortages are likely to be as important a story as AI in regard to the impact on firm profitability. Labor-intensive sectors of the economy have experienced higher inflation, primarily due to labor costs (Fig. 5). Firms that can augment labor with automation (AI or otherwise) will benefit, but those that cannot find replacements for labor will continue to see margin pressure.

Finally, we would be remiss to discuss demographics without mentioning the absurdly underfunded pension/healthcare provider we call a federal government. We’ll refrain from rehashing the long-term hurdles of our fiscal situation, but instead simply point out that the same factors are at play. Absent enough economic growth to solve our unfunded liabilities, the fiscal pie will eventually be redivided through lower benefits, higher taxes, or some combination of the two.

Fig. 5: CPI Services Inflation ex-housing

Source: Bloomberg, Mill Creek. As of 4/29/2026.

Disclosures & Important Information

Any views expressed above represent the opinions of Mill Creek Capital Advisers ("MCCA") and are not intended as a forecast or guarantee of future results. This information is for educational purposes only. It is not intended to provide, and should not be relied upon for, particular investment advice. This publication has been prepared by MCCA. The publication is provided for information purposes only. The information contained in this publication has been obtained from sources that

MCCA believes to be reliable, but MCCA does not represent or warrant that it is accurate or complete. The views in this publication are those of MCCA and are subject to change, and MCCA has no obligation to update its opinions or the information in this publication. While MCCA has obtained information believed to be reliable, MCCA, nor any of their respective officers, partners, or employees accepts any liability whatsoever for any direct or consequential loss arising from any use of this publication or its contents.

© 2025 All rights reserved. Trademarks “Mill Creek,” “Mill Creek Capital” and “Mill Creek Capital Advisors” are the exclusive property of Mill Creek Capital Advisors, LLC, are registered in the U.S. Patent and Trademark Office, and may not be used without written permission.