December Update: Tis the Earnings Season

Tis the Earnings Season

The end of the third-quarter earnings season provides an opportunity to evaluate the current state of the US equity market. In short, the US market:

- Remains supported by strong earnings growth,

- Continues to trade at a high valuation relative to history,

- Is concentrated from a market capitalization perspective, and

- Has priced in somewhat high expectations priced in about the future.

S&P 500 earnings continue to grow in the high single digits (Fig. 1), and equity analysts now expect additional earnings growth of 13% over the next 12 months. Earnings growth expectations have also broadened out from technology and the Magnificent Seven (Mag 7).

Fig. 1: S&P 500 Earnings Growth

Source: Bloomberg, Mill Creek.

Earnings growth for the Mag 7 was a remarkable 60% year-over-year at the end of the third quarter. However, such growth rates were bound to slow, at least until the large capital expenditures in AI during 2023 and 2024 show some return on investment. Analysts now expect 20% earnings growth for the next 12 months for the Mag 7.

The 12-month forward price-to-earnings ratio (P/E) for the S&P 500 is just over 21x. For perspective, the 1990-October 2024 average P/E has been 16.6x. We can conclude that the US market is, therefore, somewhat expensive, but the forest hides the trees. An equal-weight version of the S&P trades at just 17x earnings – essentially in-line with long-term valuations (Fig. 2). The Mag 7, which make up one-third of the S&P 500 by market cap, trade at a P/E of 30.

Fig. 2: Price-to-earnings

Source: Bloomberg, Mill Creek.

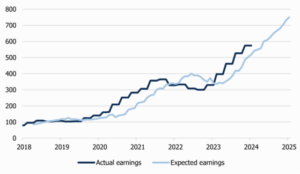

While it’s easy to look at these numbers and conclude that the Mag 7 is the place to be (e.g. better recent returns, better recent earnings growth, and higher expected earnings growth), investing is an expectations game. NVIDIA has performed well because earnings have far exceeded analyst expectations (Fig. 3), but expectations for the Mag 7 are increasingly high and ripe for disappointment.

Fig. 3: Equity Analysts Have Consistently Underestimated Mag 7 Earnings

Source: Bloomberg, Mill Creek.

The ongoing strength of the US economy is reflected in solid corporate profit growth. We remain constructive on US equity market performance, and we continue to hold an overweight to US equities in our target equity allocations. However, we also believe maintaining small cap and international exposure is important for mitigating the “expectations risk” inherent in the US market.

Disclosures & Important Information

Any views expressed above represent the opinions of Mill Creek Capital Advisers ("MCCA") and are not intended as a forecast or guarantee of future results. This information is for educational purposes only. It is not intended to provide, and should not be relied upon for, particular investment advice. This publication has been prepared by MCCA. The publication is provided for information purposes only. The information contained in this publication has been obtained from sources that

MCCA believes to be reliable, but MCCA does not represent or warrant that it is accurate or complete. The views in this publication are those of MCCA and are subject to change, and MCCA has no obligation to update its opinions or the information in this publication. While MCCA has obtained information believed to be reliable, MCCA, nor any of their respective officers, partners, or employees accepts any liability whatsoever for any direct or consequential loss arising from any use of this publication or its contents.

© 2025 All rights reserved. Trademarks “Mill Creek,” “Mill Creek Capital” and “Mill Creek Capital Advisors” are the exclusive property of Mill Creek Capital Advisors, LLC, are registered in the U.S. Patent and Trademark Office, and may not be used without written permission.