Why Is the Buffett Indicator So High?

Why Is the Buffett Indicator So High?

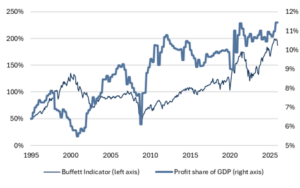

In 2001, Warren Buffett discussed a gauge for stock market valuation that is now referred to as the Buffett Indicator. It is the ratio of the market cap of the US stock market divided by US Gross National Product (GNP).1 At the time, Buffett suggested that a ratio over 120% indicates that the stock market is overvalued. Today the indicator stands at over 200% (Fig. 1). Is it possible to rationalize such a number?

If the Buffett Indicator is high, it could be because:

- The market is expensive (valuations are high), or

- Corporate profits have increased as a percentage of total economic growth.

To cut to the punchline, both of these factors are responsible for the long-term increase in the Buffett Indicator, but nearly everyone focuses on valuations and ignores the second part. Corporate profits have grown faster than labor income, which means a larger share of economic growth is coming from corporate profits than wages and salaries (Fig. 2).

Higher profit share enables a higher Buffett Indicator, all else equal, but demographics, deglobalization and artificial intelligence (AI) bring a tension into the analysis. Slowing population growth and deglobalization would generally benefit for labor (wage growth) over corporate profits, but AI could lead to higher employee productivity and offset those trends.

1 GNP is the market value of all goods and services produced by a country’s residents and businesses in a specific period, regardless of where the production occurs. It is effectively Gross Domestic Product plus overseas income earned by US companies minus income earned by foreign corporations.

Fig. 1: Buffett Indicator (United States)

Source: Bloomberg, Mill Creek. As of 3/31/2026.

Fig. 2: Corporate Profit Share of US GDP

Source: Bloomberg, Mill Creek. As of 3/31/2026.

Disclosures & Important Information

Any views expressed above represent the opinions of Mill Creek Capital Advisers ("MCCA") and are not intended as a forecast or guarantee of future results. This information is for educational purposes only. It is not intended to provide, and should not be relied upon for, particular investment advice. This publication has been prepared by MCCA. The publication is provided for information purposes only. The information contained in this publication has been obtained from sources that

MCCA believes to be reliable, but MCCA does not represent or warrant that it is accurate or complete. The views in this publication are those of MCCA and are subject to change, and MCCA has no obligation to update its opinions or the information in this publication. While MCCA has obtained information believed to be reliable, MCCA, nor any of their respective officers, partners, or employees accepts any liability whatsoever for any direct or consequential loss arising from any use of this publication or its contents.

© 2025 All rights reserved. Trademarks “Mill Creek,” “Mill Creek Capital” and “Mill Creek Capital Advisors” are the exclusive property of Mill Creek Capital Advisors, LLC, are registered in the U.S. Patent and Trademark Office, and may not be used without written permission.